US Dollar falls following Fed meeting, BoE’s Forbes calms rate cut talk

- Back to all posts

- Latest

23 September 2016

Senior Market Analyst at Ebury. Providing expert currency analysis so small and mid-sized businesses can effectively navigate international markets.

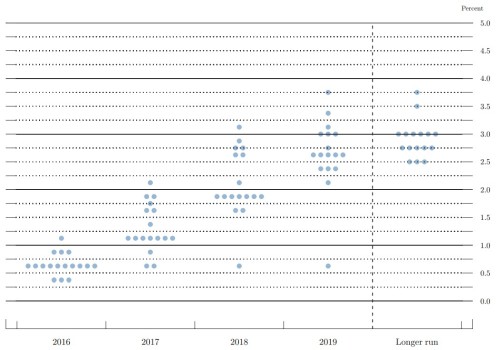

The US Dollar declined across the board yesterday after Wednesday evening’s Federal Reserve meeting suggested that the central bank in the US could be on course to hike interest rates more gradually than originally expected.

Figure 1: Federal Reserve September ‘Dot Plot’

In the UK, the Pound rose to its strongest position so far this week against the Dollar after Bank of England rate-setter Kristin Forbes claimed she saw no need for further economic stimulus from the central bank following the Brexit vote. This comes in sharp contrast to rhetoric from a number of her fellow MPC colleges that suggested interest rates in the UK could be cut to near zero in the coming months.

Elsewhere, the Norwegian Krone ended the day as one of the world’s best performing currencies yesterday after Norway’s central bank, Norges Bank, was resoundingly less dovish than expected at its monetary policy meeting. Norges Bank left its main interest rate unchanged while abandoning its expectation for further rate cuts following a string of unexpectedly strong inflation data.

Attention in the currency markets this morning was on the latest Eurozone PMI numbers, which turned out fairly underwhelming. The preliminary services and manufacturing PMIs both slowed this month to 52.1 and 52.6 respectively. We think this heaps further pressure on the European Central Bank to increase its stimulus programme in the coming months.

Major currencies in detail:

GBP

Sterling rallied for the second day on Thursday, ending the London session 0.1% higher against the US Dollar.

Expectations for another rate cut in the UK have calmed in the past couple of days, providing decent support for the Pound.

Notorious hawkish MPC member Kristin Forbes appeared unconvinced about the need for an additional rate cut, claiming that the recent ‘extremely volatile’ survey data in the UK was likely to be driven by political rather than economic news.

This follows comments from new MPC member Michael Saunders on Wednesday that claimed the fallout from the Brexit vote would prove only ‘modest’.

With no economic data out of the UK today, investors will instead look to next week’s revised second quarter GDP numbers as the next major event in the UK economy.

EUR

The Euro benefitted from Dollar weakness yesterday, rallying 0.15% against the Greenback.

President of the European Central Bank Mario Draghi spoke in Frankfurt on Thursday, although disappointed investors by failing to talk on the topic of monetary policy.

We also had the latest consumer confidence data from the European Commission, which edged higher in September. The flash estimate of the index rose to -8.2 this month from -8.5 in August, ending a run of three declines as consumers seemingly brushed aside concerns stemming from the recent Brexit vote.

This morning’s PMIs were the only major event in the Eurozone today.

USD

The US Dollar fell 0.1% against its major peers on Thursday on expectations for a more gradual path of interest rate hikes by the Federal Reserve.

Economic data out of the US yesterday was also very mixed. Initial jobless claims continued to suggest that the labour market is performing well, with claims falling more than expected to its lowest level since July. Claims fell by 8,000 to 252,000, only modestly above the four decade low 248,000 reached in April.

By contrast, existing home sales dipped in August. Sales fell 0.9% to 5.33 million, with inventory of homes for sale continuing to shrink in the US.

Today looks set to be a relatively quiet end to the week in the US with the manufacturing PMI at 14:45 UK time the only major economic release.

Receive these market updates via email

SHARE