Sterling plunges to five week low, Fed expected to hold rates steady

- Back to all posts

- Latest

21 September 2016

Senior Market Analyst at Ebury. Providing expert currency analysis so small and mid-sized businesses can effectively navigate international markets.

The Pound fell sharply to its weakest position against the US Dollar in five weeks on Tuesday on the back of growing concerns that Britain’s pending exit from the European Union could weaken the UK economy and cause the Bank of England to cut interest rates to near zero this year.

Meanwhile, the US Dollar steadied itself yesterday, with investors in a cautious mood ahead of this evening’s Federal Reserve meeting. The Fed’s Federal Open Market Committee (FOMC) will announce its interest rate decision at 19:00 UK time this evening, with Chair Yellen’s press conference to follow 30 minutes later.

We are in line with the general market consensus and expect no change in policy from the Fed tonight. We do, however, expect a more upbeat and hawkish tone during Yellen’s press conference and look for any clear hints that an interest rate hike could be on the way in the coming months. An explicit hint of a December hike would no doubt provide good support for the US Dollar against almost every major currency this week.

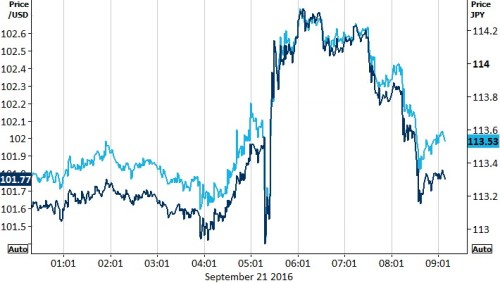

The Japanese Yen briefly fell sharply by over 1% in the early hours of this morning after the Bank of Japan announced its highly anticipated monetary policy decision (Figure 1).

Figure 1: USD/JPY & EUR/JPY (21/09/2016)

Following its comprehensive review, the BoJ will introduce an interest rate target for 10-year government bonds, committing to keep them around zero in order to stave off the threat of deflation. The main interest rate and quantitative easing programme will remain unchanged, although the QE programme will now run until inflation ‘exceeds’ rather than ‘reaches’ its 2% target.

Major currencies in detail:

GBP

Sterling continued to edge towards its multi-decade lows on Tuesday, ending 0.5% lower against the US Dollar as attention remained on Britain’s future outside the EU.

Yesterday PM Theresa May looked to increase confidence in the UK post-Brexit vote. Speaking in New York, May urged the United States to continue investing in Britain despite the shock vote to leave the EU.

This followed earlier comments from Germany’s Bundesbank on Monday that claimed financial institutions in Britain would lose so-called ‘passporting rights’ (allowing them to operate in the EU) unless the UK be part of the European Economic Area (EEA).

The Bank of England’s quarterly bulletin at midday today could receive some attention, although Sterling will likely be driven predominantly by tonight’s Fed announcement.

EUR

The Euro’s rally on Tuesday morning proved shorted lived, with the single currency ending 0.1% lower for the day against the US Dollar.

Economic news out of the Eurozone was limited yesterday, with the Euro largely driven by technical factors and expectations for the Fed meeting tonight.

ECB policymaker and senior member of the Governing Council Peter Praet spoke in Frankfurt, warning that Germany was in need of reform in order to alleviate its heavy dependence on domestic demand. This could entail introducing higher wages, increasing investment or lowering taxes.

Mario Draghi will be speaking in Frankfurt on Thursday with the latest PMIs set to be released on Friday morning.

USD

The US Dollar recovered over the course of London trading yesterday to end 0.2% higher against its major peers.

Housing data out of the US economy yesterday took a surprising turn for the worse, providing further evidence that the Fed is unlikely to hike interest rates this evening. Housing starts fell more than expected in August to 1.142 million from 1.212 million while building permits dipped by 5,000 in the month to 1.139 million. Bad weather in the South last month accounted for much of the decline and could therefore prove a one off.

The Federal Reserve meeting will undoubtedly be the highlight today and presents the greatest event risk in the currency markets this week.

Receive these market updates via email

SHARE