Sterling plunges to multi-decade low, emerging market currencies rally as Trump’s chances fade

- Back to all posts

- Latest

3 October 2016

Chief Risk Officer at Ebury. Committed to mitigating FX risk through tailored strategies, detailed market insight, and FXFC forecasting for Bloomberg.

The Pound fell sharply this morning, skidding back to a three year low against the Euro and near a three decade low versus the US Dollar after Theresa May claimed on Sunday that Article 50 would be triggered before the end of March 2017.

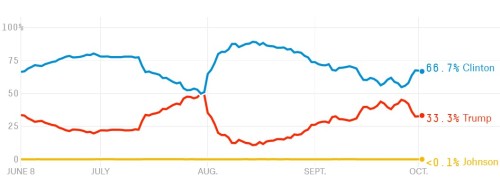

The Peso benefited from Trump’s disastrous debate performance and the ensuing fall in the polls, with Clinton now the firm favourite to win the US Presidential Election (Figure 1).

Figure 1: FiveThirtyEight US Presidential Elections Odds (June ‘16 – Oct. ‘16)

The Peso and the Ruble were also buoyed by the OPEC agreement to curb output and the subsequent sharp rise in oil prices. We have been quite bullish on both currencies for some time and it’s pleasant to have our views validated by last week’s rally. We think the currencies still have plenty of room to increase further.

The main news out of Europe last week was the concerns about Deutsche Bank’s capital position, as reflected in the volatility of its share price. We do not see any serious danger of a banking crisis, given DB’s relatively clean balance sheet, access to liquidity from central banks and the likelihood that the US penalty from misselling mortgages in the 2008-9 crisis will be much lower than the initial headline. Currency markets seemed to agree with our view and the Euro essentially ignored the DB headlines throughout the week.

This week markets will continue to be focused on events across the Atlantic. In addition to the always critical US labour market report on Friday, the drip feed of polls on the Presidential election will be the main driver for most emerging market currencies.

Major currencies in detail:

GBP

Sterling had managed to post a modest rebound last week, in the absence of any significant news. Then over the weekend news broke that Prime Minister May intends to trigger Article 50 no later than March of 2017, which would set the clock ticking for a 2019 exit from the European Union.

The Pound promptly gave up most of its gains in late Sunday Asian trading and fell sharply this morning to less than a cent away from its 31 year low against the US Dollar.

This week we get further indicators of the resilience of the UK economy post-Brexit, in the shape of the PMI business confidence indicators.

EUR

The only macroeconomic news of note last week from the Eurozone was the flash inflation numbers for September.

The core number that excludes volatile components remained at a stubbornly low 0.8%, confounding expectations for a modest increase. The ECB is getting no relief from inflation readings and this should maintain the pressure on the council to add economic stimulus at some point in the next three meetings.

The political calendar is set to become a key driver for the Euro. This weekend’s dramatic crisis in Spain’s opposition Socialist party, which may finally enable the country to form a Government; the Constitutional referendum in Italy, with the possibility of a damaging rejection of the government’s plans; and Portugal’s ongoing argument with the Troika all will be closely watched by currency markets over the coming weeks.

USD

We expect a busy week ahead in the US.

In addition to the labor market report on Friday, which is the key to further Federal Reserve hikes, we will continue to follow closely the Presidential Election polls for confirmation that the post-debate bounce in Clinton’s numbers is holding. If so, we would expect risk assets in general, and emerging market currencies in particular, to remain well supported – though the impact on the US Dollar itself is for now unclear. The greenback so far has expressed no clear preference for either of the presidential candidates.

Receive these market updates via email

SHARE