Sterling spikes after strong services PMI fuels hope of BoE rate hike

- Back to all posts

- Latest

6 April 2017

Senior Market Analyst at Ebury. Providing expert currency analysis so small and mid-sized businesses can effectively navigate international markets.

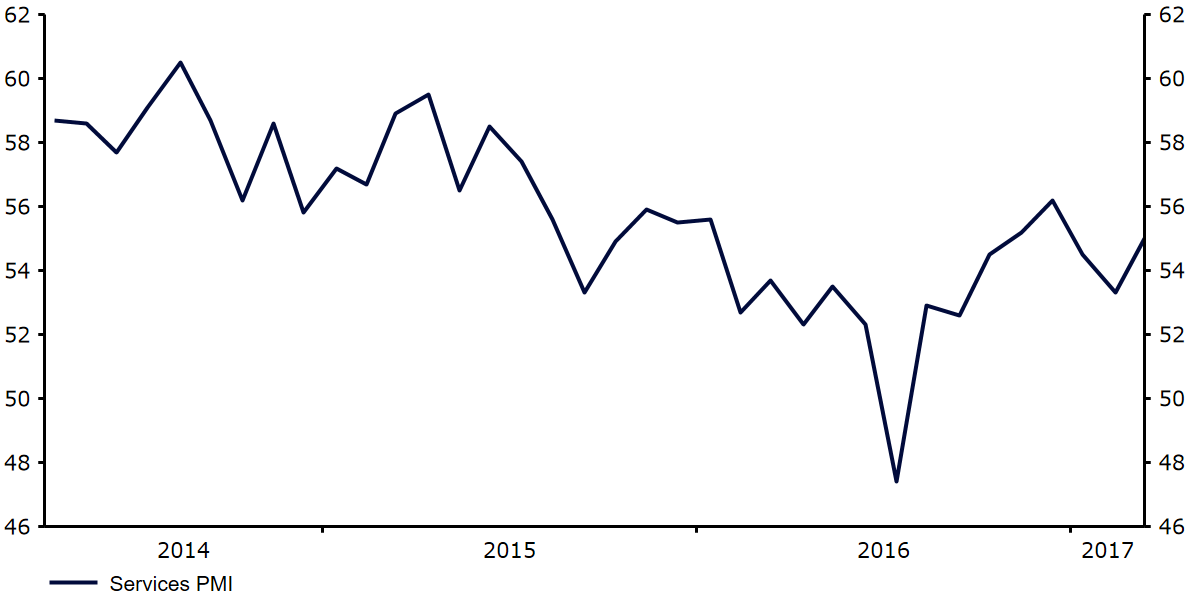

The Pound rose against both the US Dollar and the Euro on Wednesday after the latest services PMI from Markit unexpectedly increased back to its highest level in three months.

Figure 1: UK Services PMI (2014 – 2017)

The data will be welcome news to the Bank of England, given services accounts for around 70% of overall output, and will no doubt ramp up expectations that the Central Bank could be on course to raise interest rates in the UK before the end of the year.

Over in the US, the latest ADP employment report smashed expectations, boding well for tomorrow’s nonfarm payrolls data. The private sector of the US economy added 263,000 jobs in March, considerably above forecast. The downward revision in the February number was a slight disappointment, although the March number more than made up for it, providing decent support for the US Dollar across the board. While the correlation between yesterday’s number and the nonfarm payrolls data is far from perfect, the signs for a strong payrolls number around the 180-200k mark are good at this stage.

Last night, the Federal Reserve also released the minutes of its monetary policy meeting. The key takeaway was more to do with a possible balance sheet reduction this year rather than interest rate policy, and the Dollar showed little significant movement as a result.

Major currencies in detail

GBP

The Pound jumped 0.4% after yesterday’s services PMI ramped up expectations that the BoE could hike interest rates sooner rather than later.

Bank of England dove Gertjan Vlieghe was unsurprisingly slightly less supportive of the idea of higher rates on Wednesday, despite the recent improvement in economic data. Vlieghe even claimed that a slowdown in consumer activity was on the way, warning the market that the central bank should remain cautious as to the path of future interest rate hikes. He also claimed that there would need to be evidence of an inflation pick-up fuelled by factors other than Sterling depreciation before he votes for higher rates.

With no economic data out of the UK today, the Pound will likely be driven by events elsewhere.

EUR

The Euro had a mixed session yesterday. The single currency initial rose just after midday following comments from ECB member and Bundesbank chief Weidmann, who suggested he would welcome an end to the central bank’s bond purchases within the next year. Expectations that the ECB will reduce its quantitative easing programme before the end of the year grew sharply following February inflation data. We think this remains some way off given core price growth remains stuck below 1%. However, broad Dollar strength ensued following the ADP employment report and the Euro ended the session lower against the greenback.

The ECB’s meeting accounts and unrelated press conference from Mario Draghi later this evening will be the main announcements in the Eurozone today.

USD

Economic news out of the US yesterday was mixed, despite the strong labour market numbers. The ISM’s non-manufacturing PMI came in comfortably below expectations. The index declined from 57.6 to 55.2, its lowest level since as far back as October last year.

Investors now turn their attention to Donald Trump’s highly anticipated meeting with Xi Jinping this afternoon. The meeting could have widespread ramifications beyond purely trade ties and the Yuan, but also a number of other Asian currencies that rely heavily on trade links with both countries. Economic data today, including jobless claims, are likely to take a back seat.

SHARE