Euro falls on Deutsche Bank concerns, Fed Chair Yellen to testify

- Back to all posts

- Latest

28 September 2016

Senior Market Analyst at Ebury. Providing expert currency analysis so small and mid-sized businesses can effectively navigate international markets.

The Euro fell across the board on Tuesday, dipping back below the 1.12 level against the US Dollar to its weakest position since last Thursday as concerns regarding the health of the fragile European banking system came into sharp focus.

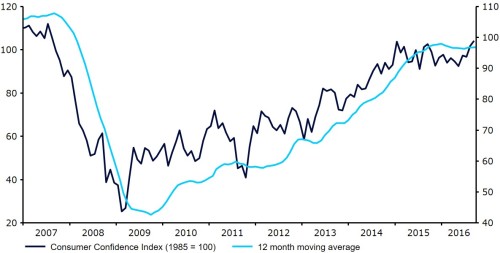

The Dollar was kept well supported yesterday following a strong set of manufacturing and confidence data, the latter of which surged above expectations to levels not seen since before the financial crisis (Figure 1).

Figure 1: US Consumer Confidence (2007 – 2016)

Investors also breathed a sigh of relief following the general consensus that Hillary Clinton came out on top in Monday night’s US Presidential Election TV debate. The Mexican Peso, which has suffered a sharp sell-off in the past few weeks following Trump’s surge in the polls, was one of the best performing currencies during the London session.

Today looks set to be a particularly busy day in the currency markets, with Federal Reserve Chair Janet Yellen beginning her two day semi-annual testimony in front of Congress at 15:00 UK time this afternoon. Yellen’s comments on monetary policy could provide clues as to the likely timing of the next US interest rate hike, with the market now firmly pricing in the possibility that rates will be raised for the second time in a year at the December FOMC meeting.

President of the European Central Bank Mario Draghi will also be speaking today in a hectic day of central bank appearances. Draghi will be speaking in Berlin at 14:30 UK time, with investors looking for hints as to the possibility of further economic stimulus in the Euro-area before year-end.

Major currencies in detail:

GBP

Sterling traded mostly under the radar on Tuesday, with limited announcements in the UK for the second straight day keeping the Pound range bound. The UK currency rose by a modest 0.35% against the US Dollar.

Retail sales in the UK suffered a setback in September according to the latest distributive trades survey from CBI. The monthly index fell unexpectedly after a strong showing in August, dipping to -8 from 9.

Economic data since the Brexit vote continues to be very mixed, leading to divisions among the Bank of England’s monetary policy committee regarding the central bank’s next move. Policymaker Kristin Forbes last week suggested that she would not vote for a further rate cut, contrary to comments from Governor Carney earlier in the month.

With no economic data in the UK today, Sterling will likely be driven by events elsewhere. Friday’s growth data will be the only major economic release in the UK this week.

EUR

The Euro fell 0.3% against the US Dollar on the back of growing concerns about the health of the European banking system.

A top official at Germany’s central bank, the Bundesbank, addressed the mounting pressure on the German banking system yesterday. Andreas Dombret claimed that political support for the banks ‘must finally come to an end’, suggesting that structural deficiencies would need to be tackled in order to ensure the health of some of Germany’s biggest banks.

German consumer confidence this morning is expected to remain unchanged. Draghi’s speech this afternoon will be the main focal point today.

USD

A weak Euro and impressive economic data sent the US Dollar index 0.2% higher on Tuesday.

The US manufacturing PMI for September exceeded expectations yesterday, increasing to 51.9 from 51.0. Consumer confidence also surprised to the upside, increasing to 104.1 from 101.8, defying expectations for a decrease.

Federal Reserve rate-setter Stanley Fischer also spoke in Washington yesterday, claiming he didn’t want interest rates to rise too much, despite improvements in the labour market.

This afternoon’s US durable goods orders data is expected to slip into negative territory following an impressive result in July. The Federal Reserve sees this as one of the key gauges of economic performance when deciding on its next monetary policy move and so the release should receive some attention this afternoon.

Receive these market updates via email

SHARE